Winter 2021

Successful vaccine rollout has allowed the UK economy to reopen

The coronavirus pandemic , and public health measures introduced by governments to prevent the spread of infection, has produced one of the largest historic shocks to the world economy. World output fell by more than 3%, with more than three quarters of the globe experiencing a fall in economic output in 2020. Recent analysis by the Office for Budget Responsibility (OBR) using IMF data showed that 86% of countries saw economic output fall in 2020. A consensus is that the global nature of the crisis has exacerbated the domestic economic situation within each country.

An early warning given by the OECD was that the pandemic is “a major economic crisis that will burden our societies for years to come.”. The IMF believed in May 2020 that at least until 2023, global economic output will not return to pre-coronavirus levels. The IMF’s chief economist said then, the world was experiencing the “worst recession since the Great Depression” of the 1930s.

Economic impact of the pandemic to date

On the eve of the UK’s withdrawal from the EU, January 2020, UK growth in output was continuing apace. Recession looked an unlikely prospect, there were record numbers of people in employment, the unemployment rate was at a historic low, earnings on average were growing faster than inflation and inflation remained steady at less than 2%. Average earnings had finally exceeded their 2008 pre-financial crisis levels. At that time in early 2020, the Treasury’s survey of independent forecasts was showing an average forecast of 1.2% GDP growth for 2020.

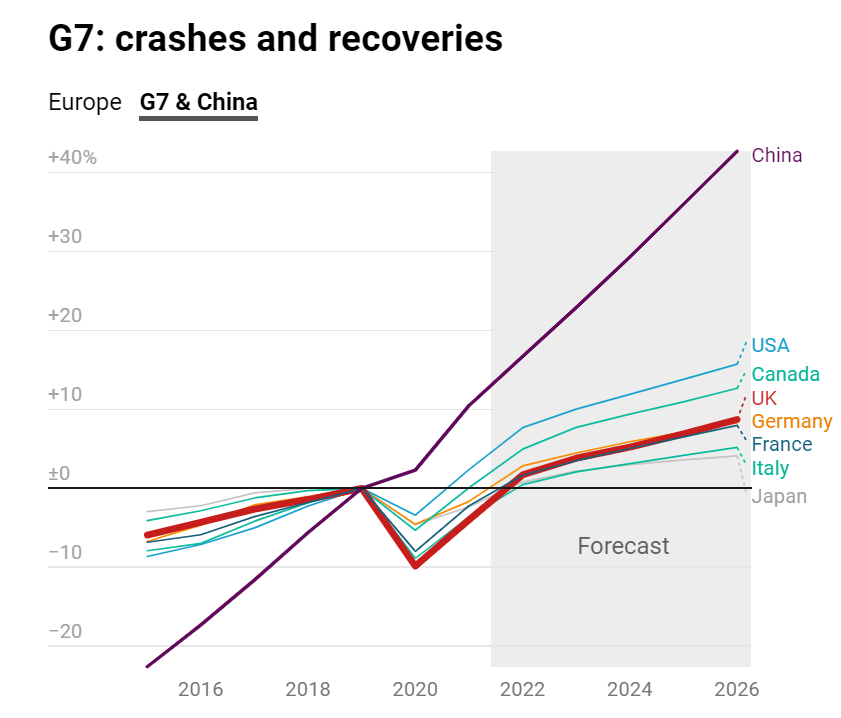

Since the first reported confirmed case of infection in the UK in January 2020, severe acute respiratory syndrome coronavirus 2 (SARS-CoV-2), which emerged from eastern China in December 2019 there was a growing interruption to the global economy. Initial disruption was to supplies of goods from the Chinese economy, the world's second-largest.

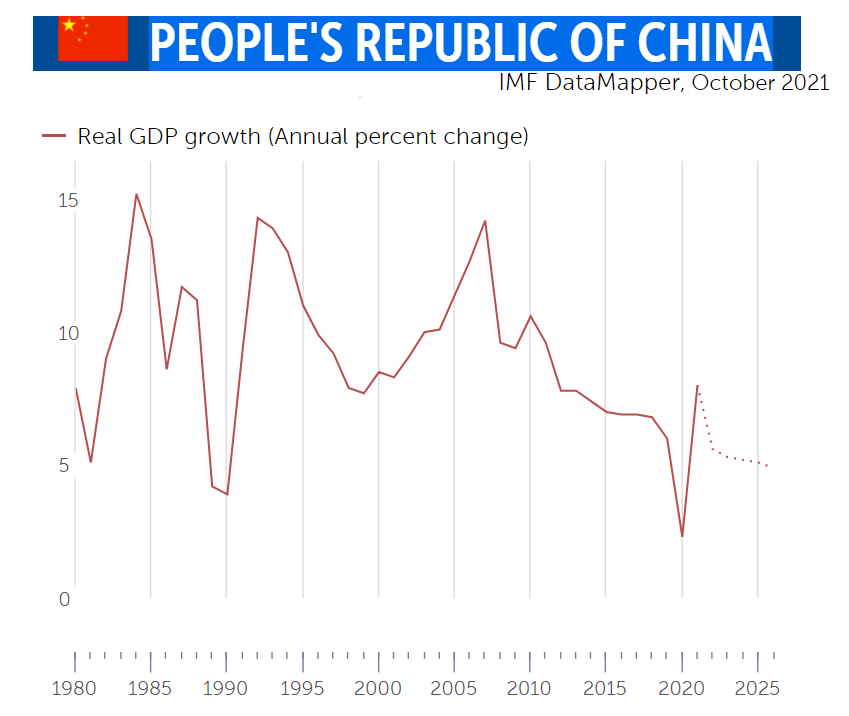

However, the Chinese economy did not then deteriorate to the same degree as the West. By the third quarter of 2020 the Chinese economy was reporting year-on-year growth (annual reported growth by the IMF is 2.3% for 2020 and 8% for 2021).

China did not suffer a second wave of infection, as experienced in the UK. Possibly owing to their ‘zero Covid strategy’, which they have persisted with, involving strict lockdowns, border control, and extensive testing and tracing of those infected.

Lately though, rising energy costs and Chinese energy rationing, owing to a pandemic-related ‘global energy crunch’, have threatened Chinese output. The Chinese economy is reliant on coal for more than half of its power and half of the coal burned in the world is burned by China. With thermal coal prices continuing to rise, this may yet presage a Chinese recession. This would be the first in 30 years.

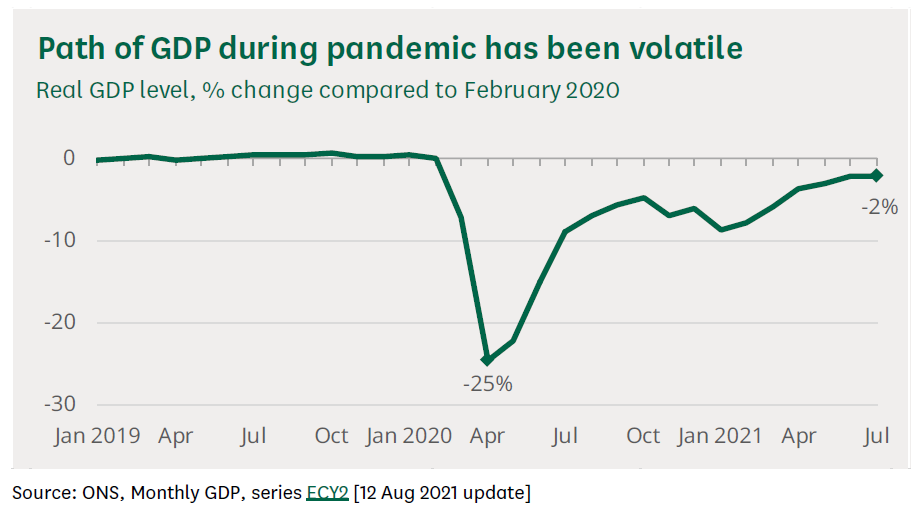

In 2020, as the outbreak of infection spread around the world and into the UK, public health measures to prevent infection saw fewer people working and some businesses in some sectors in the UK shutting. The first effect was felt in the travel and tourism sectors, which remain some of the worst affected parts of the economy. As infection spread rapidly before March 2020, people began voluntarily restricting their movements and changing spending habits. In the period immediately following the first lockdown of the UK economy on 23 March 2020, UK economic output is reported to have declined by around, an unprecedented, one quarter.

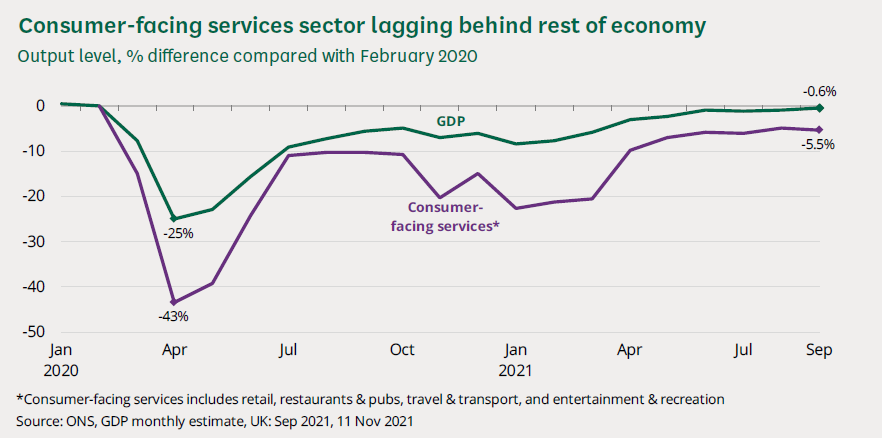

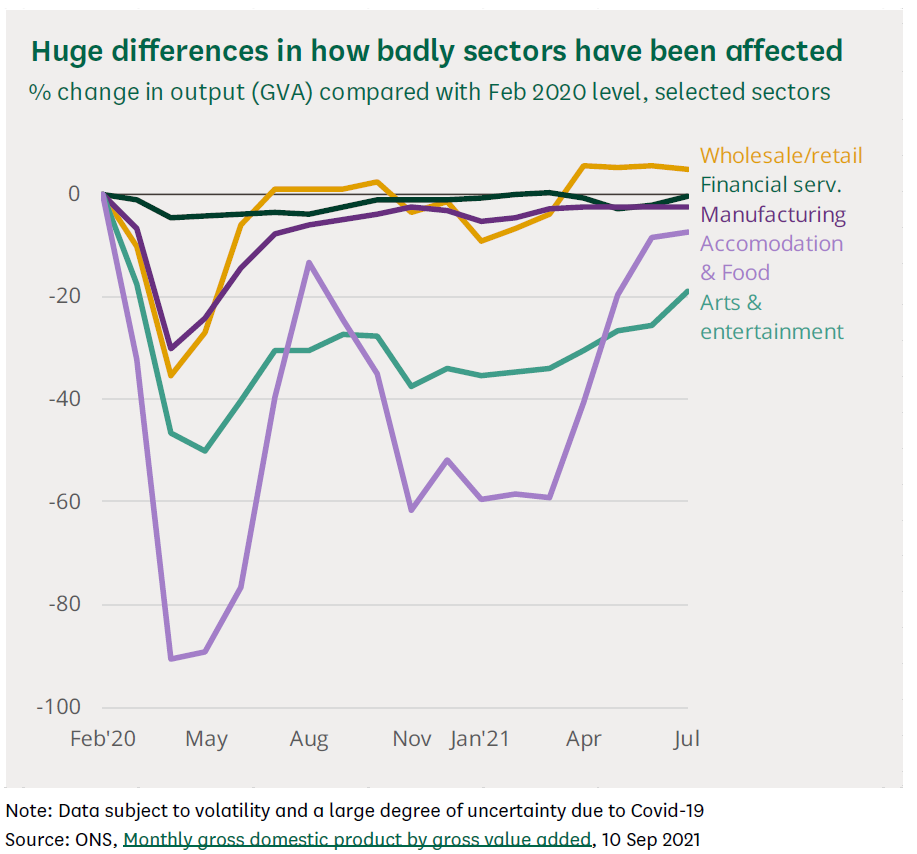

A striking feature of the pandemic is the extent to which different sectors of the UK economy have been affected to differing degrees. Unsurprisingly, sectors reliant on social contact, for example, including hospitality and entertainment, have been especially heavily affected. Accommodation and food services experienced an initial loss of output of around 90% relative to the pre-pandemic level. Whereas sectors, such as financial services, where initially output fell by 6%, have fared much better over the last eighteen months or so.

Some sectors, such as construction, where activity fell nearly by half in the first lockdown period in 2020 were around only 2% lower by the January 2021 period. Manufacturing dropped by nearly 30% and then recovered over twelve months to be 5% lower.

Nevertheless, the magnitude of recession in the UK owing to the pandemic is unprecedented.

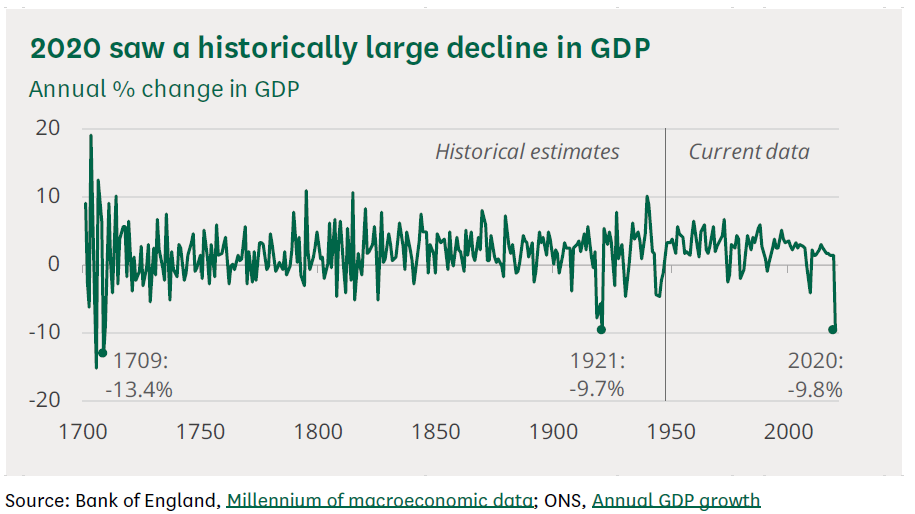

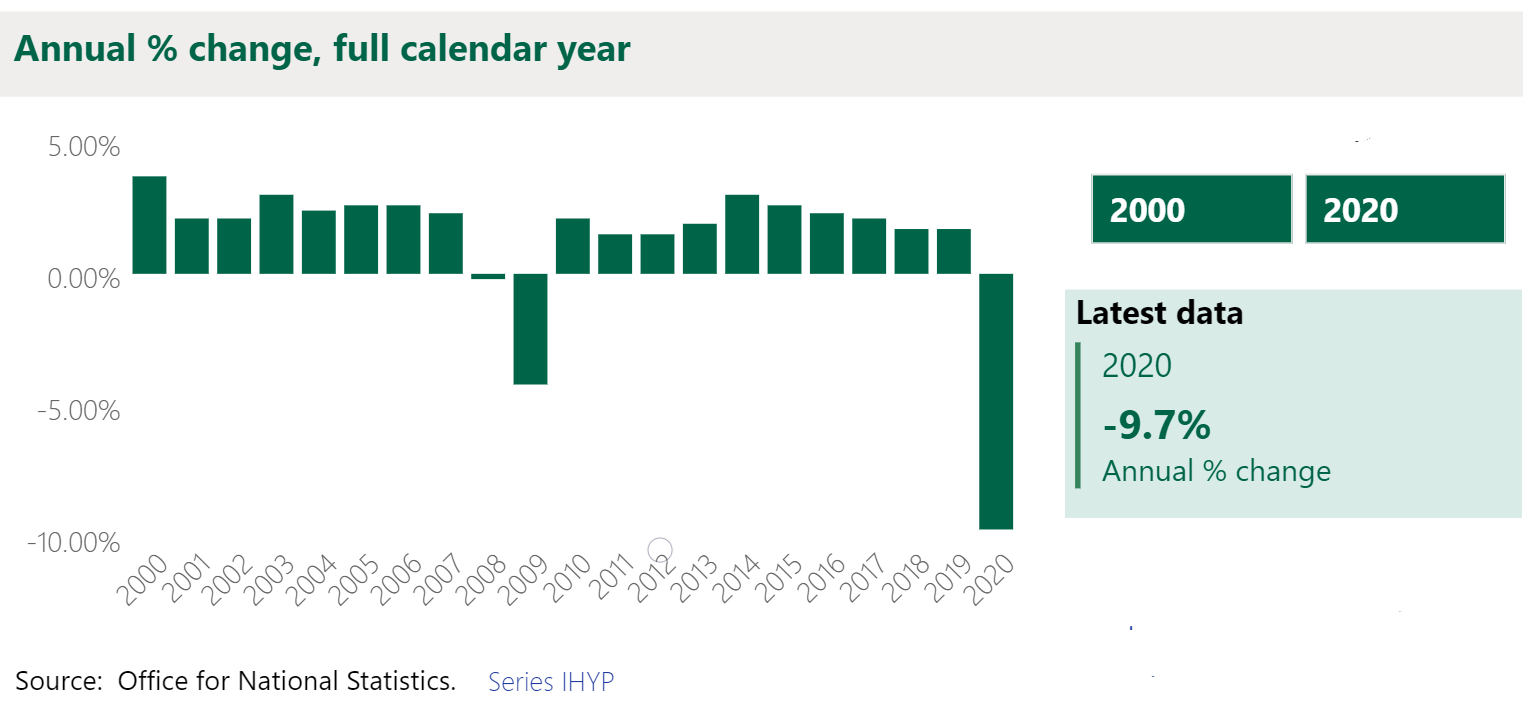

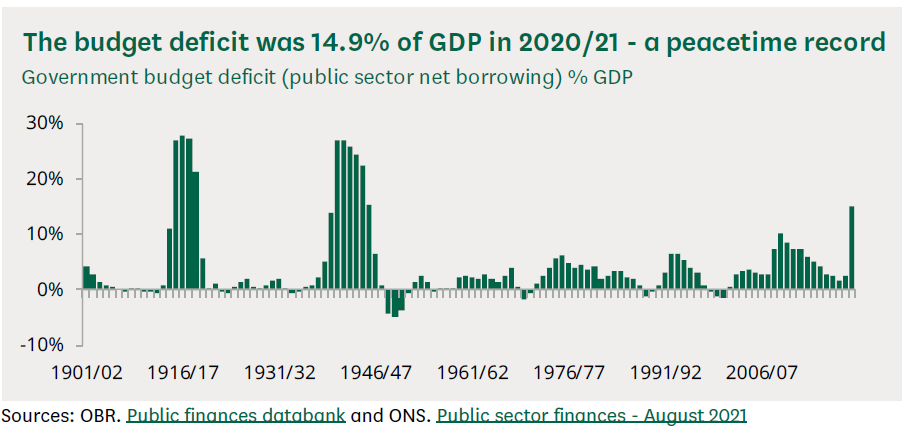

The measure of economic output maintained by the Office for National Statistics, UK Gross Domestic Product (GDP), declined in total by nearly 10% in 2020. The steepest reversal of recorded economic activity since consistent records began after WWII in 1948; probably the largest drop in output since 1921; almost twice the size of recession in the wake of the 2008 financial crisis.

UK output for last twenty years

Where output reduced by around a quarter in April 2020, it was 9% lower by January 2021, even though each of these periods was during ‘full national lockdown’, and the January 2021 nadir.

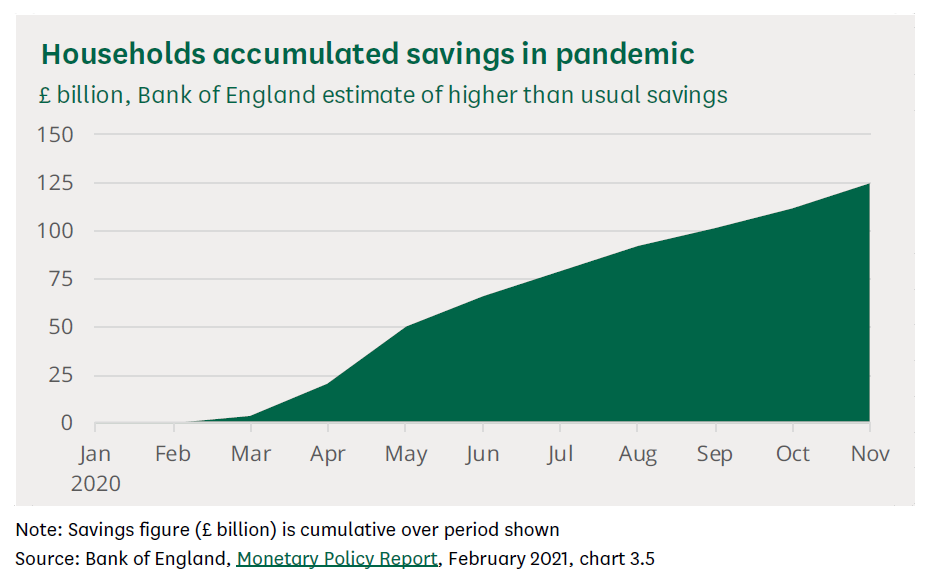

UK economic decline in the winter of 2020-21 was much less severe than during the first lockdown, as businesses adapted, and consumers changed their habits. The reduction in mobility and opportunity for consumers to spend led to the savings rate of households rising from around 7% to 26%.

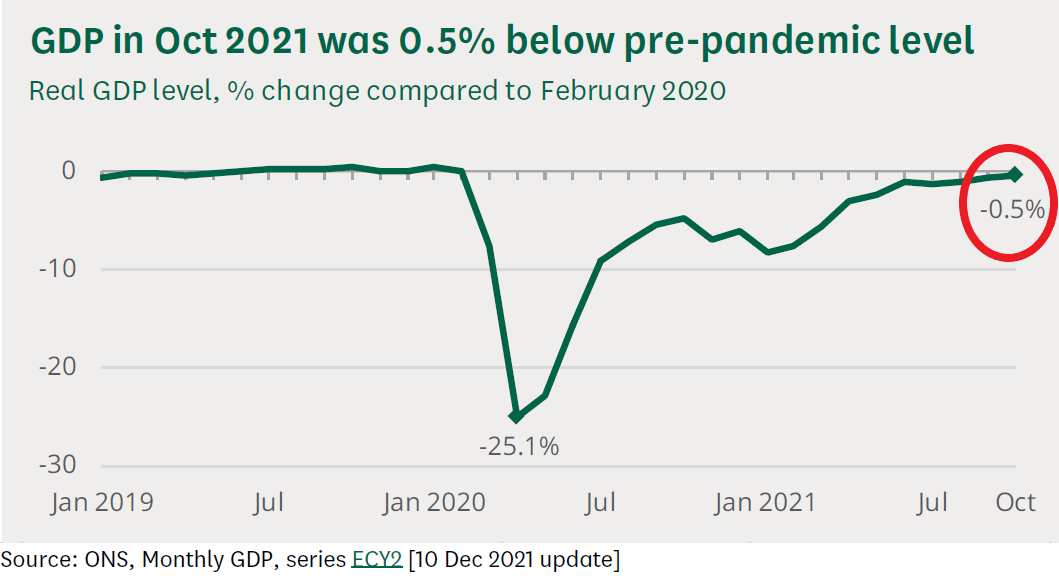

What followed was a strong recovery, particularly in consumer spending, in spring and summer 2021, with a rebounding of UK output, which now is tantalisingly only ½% lower than before the pandemic.

The early 2021 lockdowns were stricter than November 2020, but not as strict as those introduced in March 2020. For instance, more businesses stayed open, and consumers and businesses had adapted to an extent to working and shopping from home.

The surge in online sales, which accounted for a record 37% of total retail spending in February 2021, up from 20% in February 2020 has since fallen to stand at 28% in August 2021.

Uncertainty and optimism

The pandemic has created significant uncertainty, not least about the length of the crisis. This uncertainty in and of itself has affected consumer and business confidence and behaviour. Businesses facing a squeeze on their cash reserves during the lockdowns reduced investment in part due to the uncertain economic outlook.

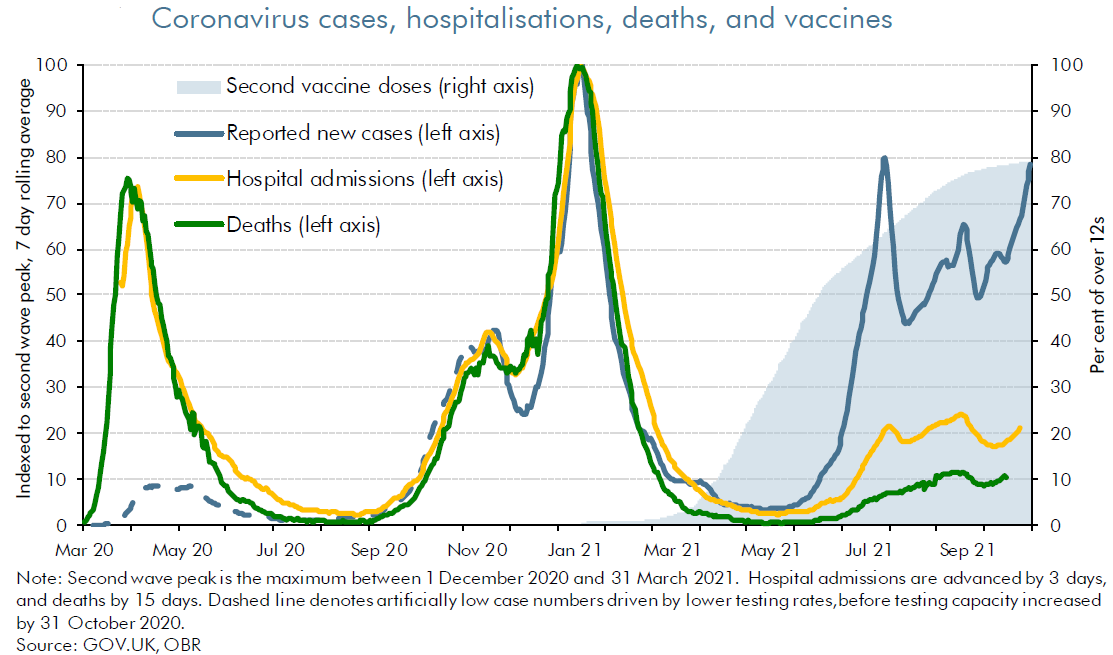

The UK’s vaccination programme during 2021 seems to have reduced some of this uncertainty, despite the spread of new variants. Optimism over the economic outlook developed during this year as virus caseloads fell and remained consistently lower than in either March 2020 or January 2021, as the numbers of people receiving the Covid-19 vaccines has consistently risen. However, epidemiologically, heading into the winter of 2021-22, uncertainty persists even though more than 51 million people in the UK have received their first vaccine dose: around 90% of the general population (aged 18 to over 80). Nearly 47 million of these have received two doses. Cases of the virus, however, are now relatively high (nearly 55,000, as against 61,000 in January 2021) and increasing.

Forecast

On October 27th 2021 Chancellor Rishi Sunak unveiled an autumn Budget in the House of Commons and presented the OBR’s economic and fiscal outlook. The OBR closed making their forecast earlier than usual to provide the Chancellor with a stable basis on which to complete the Spending Review negotiations, the first of its type in six years. In their latest forecast while they expect an increase in infections to lead to restrictions over the winter, they assume there is no return to a nationwide lockdown.

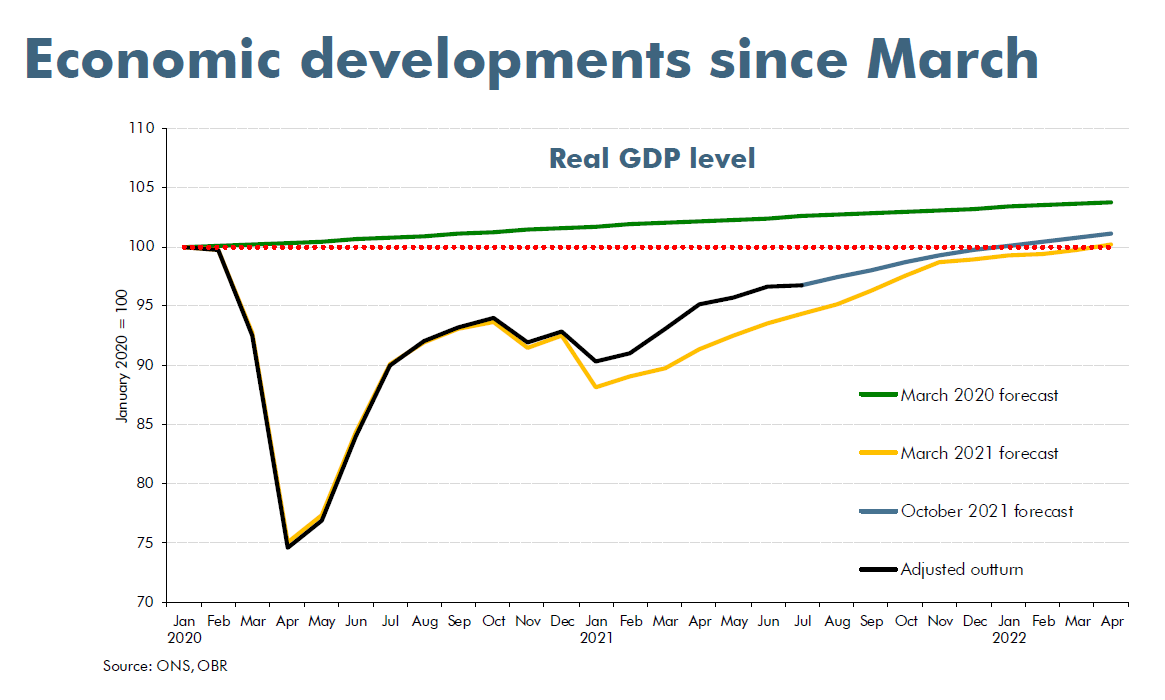

A comparison between their March and October forecasts is that they overestimated the fall in output associated with the last lockdown. The latest data shows with the summer surge in demand that output fell by just nearly 1½% in the first quarter of this year as opposed to the 4% they had assumed. This continues a pattern of underestimating, by the OBR, the adaptability of the UK economy.

The summer surge in demand took output to around 1% below the pre-pandemic level of output (by August 2021). A strong rebound in the appetite for consumption created challenges in satisfying demand. Supply constraints for goods and labour have continued into the autumn. The OBR expect growth of 6½% this year and for the economy to be the same size as the pre-pandemic level around the end of the year. Much earlier and stronger than the OBR had previously forecast.

Inflation

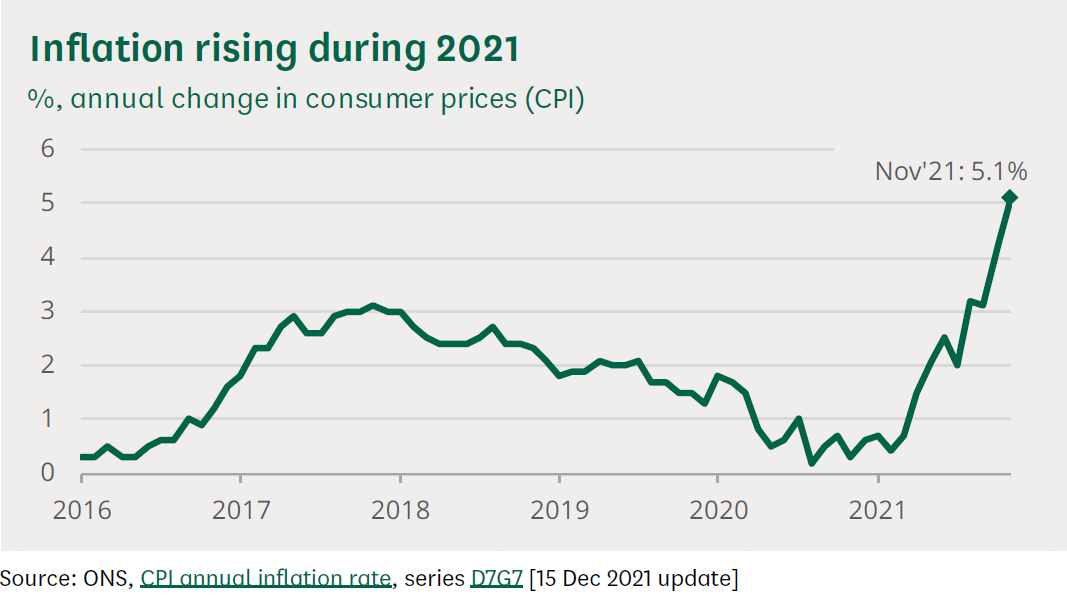

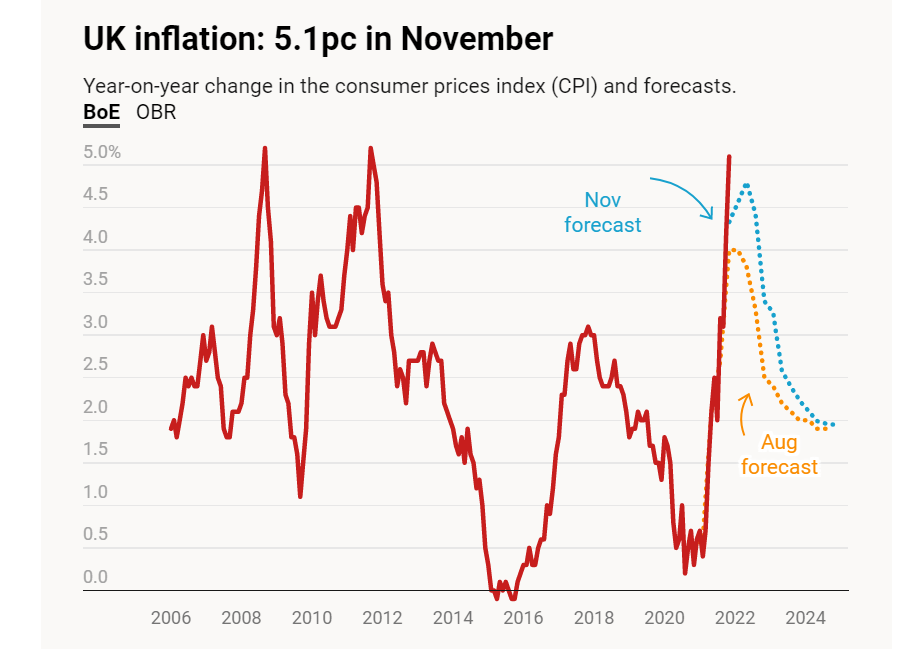

The combination of this strong rebound and constrained supply, in the UK and internationally, has led to a general and marked increase in price inflation. Strong demand from consumers for goods and higher labour costs for businesses are being reflected in higher prices. Already CPI inflation is now over 5% and rising, much higher in November 2021 than a year before: last year inflation was under 1% and stable, at the end of 2020, and into the first few months of this year. On a monthly basis, CPI increased by 0.7% in November 2021, compared with a fall of 0.1% in November 2020.

The CPI statistic is already standing at the highest 12-month rate, in over ten years, since September 2011. This makes the OBR’s latest expectations look unrealistic: with the OBR expecting in their forecast for CPI inflation to peak at close to 4½% by middle of next year and thereafter gently fall back to the Bank of England’s target.

A main source of price inflation is owing to the rising cost of energy. In December, Dr Broadbent, an economist, and previous member of the Bank of England's Monetary Policy Committee (MPC), a Deputy Governor with specific responsibility for the Bank’s monetary policy stated that "… inflation is likely to rise further over the next few months and… comfortably exceed 5%...” when the statutory price-cap on retail energy prices is next adjusted next April, 2022. Apparently, commentators predict an almost certain increase in the price-cap in April ‘22, possibly by another 30%, since the formula is based on wholesale energy prices, which have recently risen by around 250%.

The RPI inflation rate was 7.1% in November 2021, up from 4.9% in September.

Concerns for sharply rising inflation may have prompted the Bank’s Governor to lead the City to form the view that the base rate would rise from 0.1 per cent to 0.25 per cent at the November meeting of the MPC. Apparently, traders adjusted their positions and some mortgage lenders raised terms accordingly. But in the event seven of nine committee members, including the Governor, rowed back on this, and voted ‘no change’ — provoking market volatility and much criticism for his signalling. But now, on 16 December, in a surprising move, the MPC voted (8-1 in favour) to increase base rate to 0.25%!

Labour Market

An unambiguously positive effect of the strong summer recovery has been the UK economy drawing over 3 million people from furlough in just over six months, leaving around 1.3 million at the scheme’s closure in September. With continuing strong demand for labour in the UK economy, there are a record 1.22 million vacancies advertised in the three months to November 2021, an increase of over 400,000 on the pre-pandemic January-March 2020 level, with 15 of the 18 industry sectors showing record highs. Cautiously, perhaps over cautiously given current data, the OBR assume a ‘modest uptick’ in unemployment by the end of 2021. Nevertheless, a much lower figure than they had previously been predicting.

According to early evidence from HMRC there is to be expected only a limited effect on the overall unemployment rate following the end of the furlough scheme. The number of pay-rolled employees (excluding self-employed) were up by 160,000 in October, compared with September 2021 and have continued to increase month-on-month in November 2021 by 257,000 and are now 446,000 above the pre-pandemic levels of March 2020.

Last November 2020, the OBR expected unemployment to rise by more than 800,000. The combined effect of Government’s measures and business adaptation has successfully ensured that unemployment is much lower than might have been expected. A recent study (October 2021) conducted by the ONS has found that 87% of furloughed employees returned to work and 3% have been made redundant.

The ONS report 32.51 million people were in employment between August and Oct 2021. In 2019, the labour market ended that year with the highest employment rate of 76.5% or 32.99m people and joint-lowest unemployment rate of 3.8%, since comparable records began in 1971. Last year the ONS reported 32.39 million people were in employment in October-December 2020, down 541,000 from the year before. Employment levels have risen over the past quarter and the past year, although are still 500,000 less than their pre-pandemic level. The extension of the furlough scheme and rebounding economy has ensured that the rise in the number of jobseekers of over ½ million that was expected by the OBR has been limited.

The OBR had inferred in their last projection that around 2¼ million people would be out of work at the end of 2021. That ‘peak’ the OBR had projected, never materialised.

In August-October 2021, there were 1.42 million unemployed people in the UK. The unemployment rate (the percentage of the economically active population who are unemployed) is 4.2%. Unemployment levels have fallen over the past quarter and have almost returned to pre-pandemic levels.

Medium-term economic outlook

The OBR’s five-year viewpoint has adjusted in their latest report to reflect a more positive stance, owing to a stronger recovery in output and resilience in employment. Rather than expect a permanent reduction in the capacity of the UK economy of 3% GDP they have revised this to 2% GDP. The OBR now expect continued strong real growth into next year where GDP is expected to settle down to the trend growth rate of around 1¾%. The OBR say that higher real growth over the medium term coupled with higher inflation in the near term will mean nominal output will be substantially higher leading to additional ‘fiscal drag’ caused by the March 2021 Budget’s five-year freeze in the income tax thresholds.

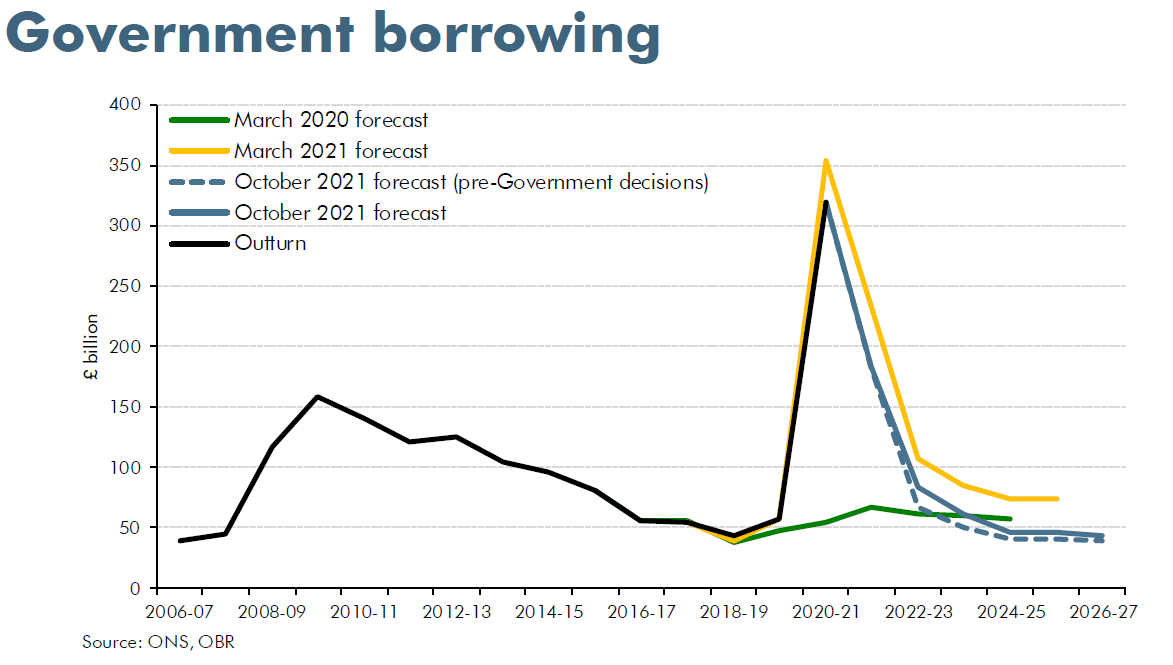

Government borrowing and debt

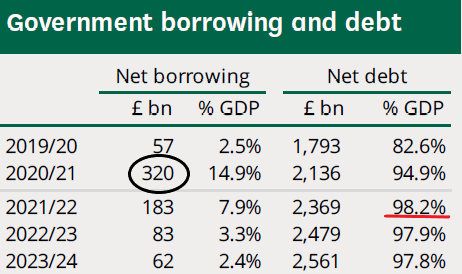

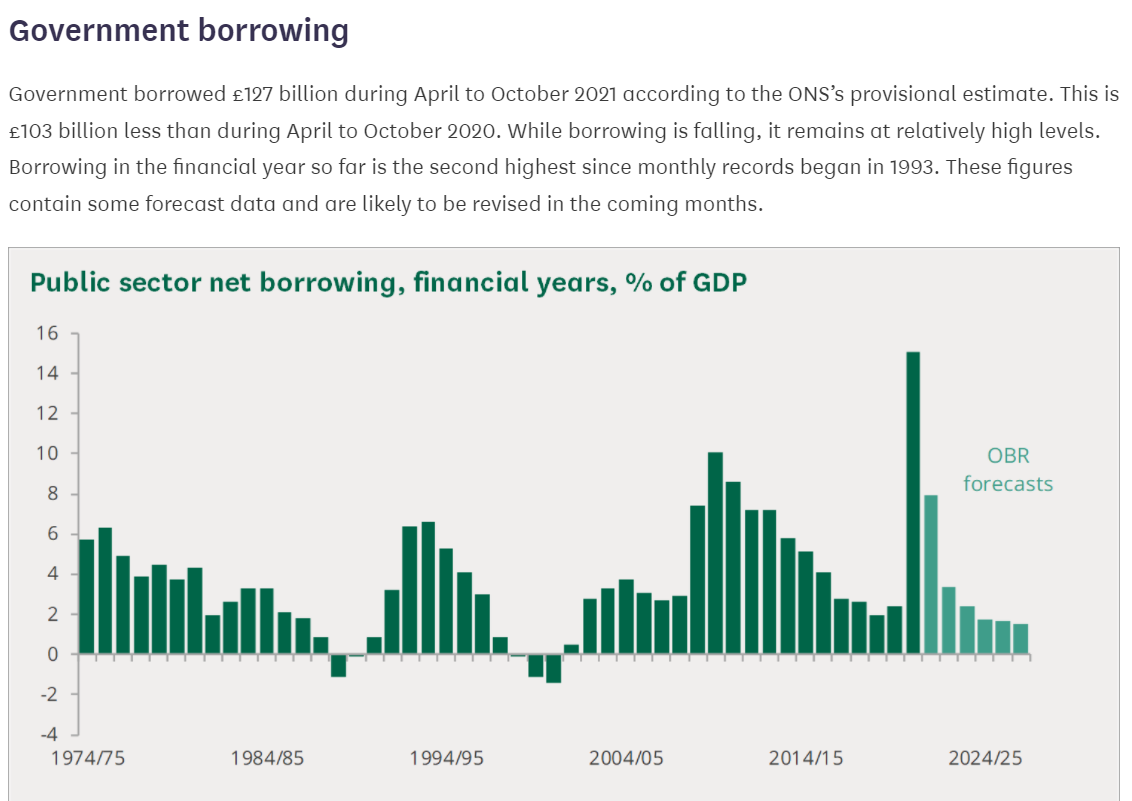

Based on the OBR’s latest forecast, borrowing will still peak at a post-war high of £320 billion or 15% of GDP in the last fiscal year, although £35 billion lower than previously expected. Higher growth and inflation push up receipts by around £50 billion a year but also spending on welfare, debt interest, and other items by around £15 billion a year. On top of this £35 billion the Chancellor has raised a further £15 billion a year in net tax increases, most notably in the guise of the new health and social care levy announced in September 2021. Of this extra £50 billion a year of additional revenue to deploy in this Budget and Spending Review, the Chancellor has allocated around £30 billion: half is to go from the new levy into the NHS and social care budget; the other half undoes cuts to departmental spending pencilled in at the start of the pandemic. The remaining £20 to £25 billion a year in extra revenue is used to reduce borrowing.

The roughly £25 billion a year left from the Spending Review is, the OBR project, sufficient to stabilise the debt-to-GDP ratio just below 100% of GDP.

Taxation

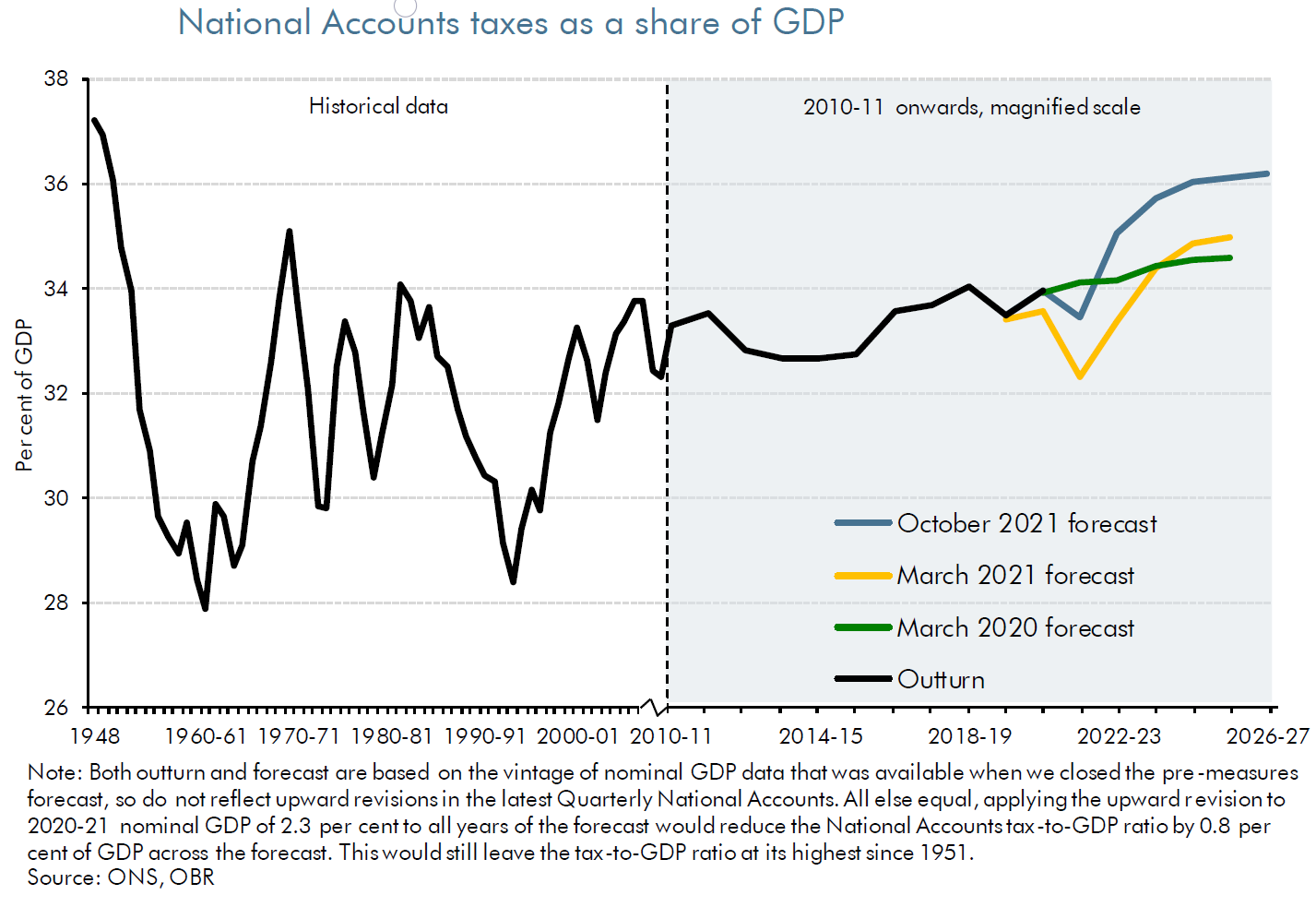

The OBR point out the scale of tax announcements the Chancellor has made this year, which they say is ‘hard to underestimate’: arising from the combination of corporate and personal tax rises announced in March, September, and in the October Budget means that this Chancellor has announced more tax rises this year than in any single year since Norman Lamont and Ken Clarke’s two 1993 Budgets in the aftermath of Black Wednesday.

Of these tax rises, coupled with fiscal drag, the overall tax burden is expected to rise from 33½ per cent of GDP pre-pandemic to above 36% of GDP in five years time. If this happens then this would be the highest level of taxation since the tail-end of Clement Attlee’s Government in the early 1950s. The OBR estimate that one-third of the announced increase in taxation comes from the fiscal drag in the tax system the Chancellor inherited from his predecessors. Another one-third comes from cancelling the planned 2% corporation tax cut (March 2020 Budget) and the further increase in the main rate of CT from 19% to 25%, announced in March this year, 2021. About one-fifth comes from the freezing of personal tax allowances and thresholds also announced in the March Budget. And another fifth comes from the new Health and Social Care Levy announced in September.

Public spending

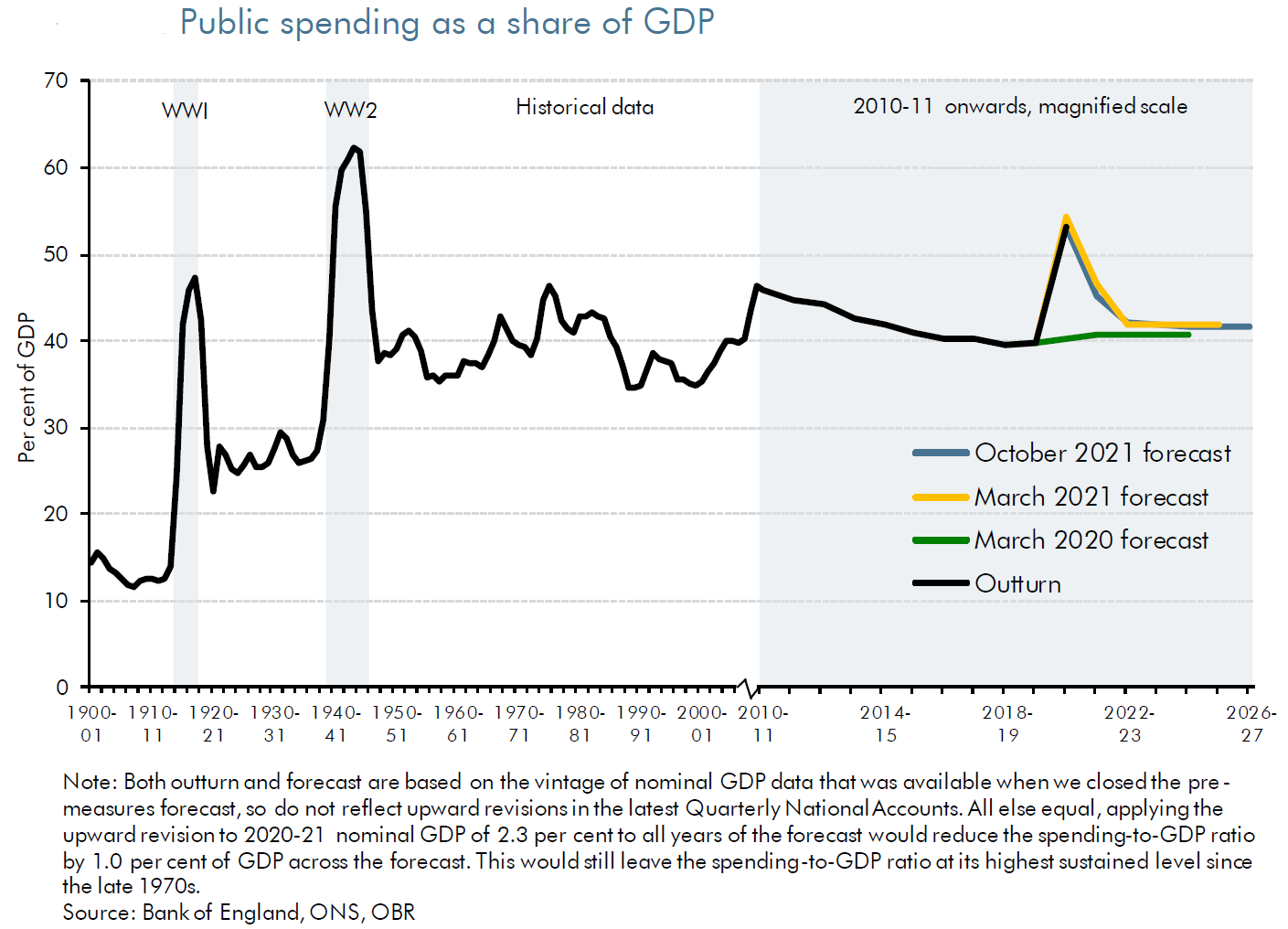

In terms of spending, the Chancellor uses 60% of the increase in revenues relative to the OBR’s last forecast to permanently increase the size of the post-pandemic state in his three-year Spending Review.

While public spending falls back from the peacetime high of 53% of GDP last year as pandemic support is withdrawn, the forecast has this settle at just below 42% of GDP in the final three years of the forecast period. This will be nearly 2% of GDP higher than before the pandemic and takes the size of the state to its highest sustained level since the late 1970s, and before the privatisations of the 80s and 90s.

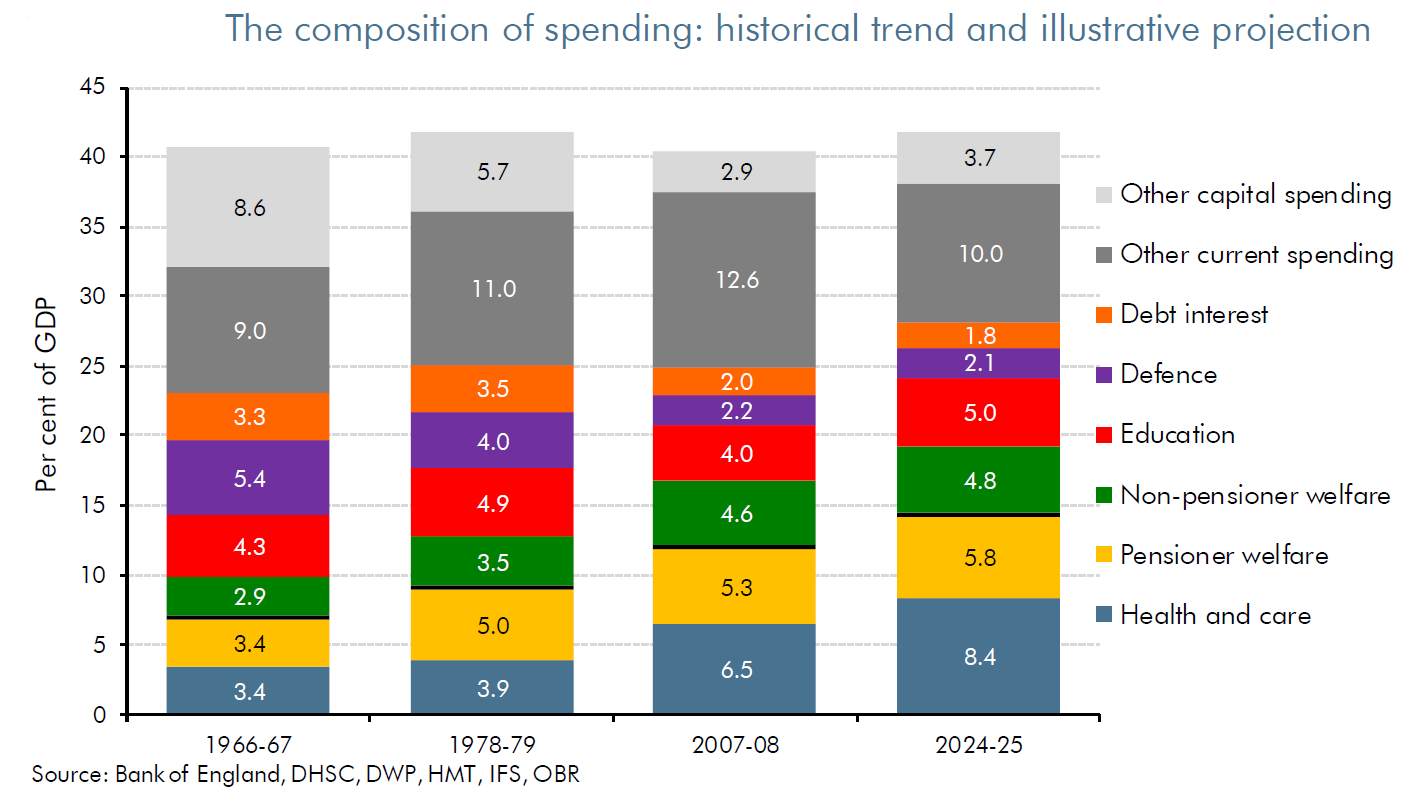

The UK will be spending 60% more of our national income on the NHS, social care, and pensions, reflecting the increase in the share of the population over 65 from one-in-seven of us in the late 1970s to one-in-five of us by the middle of this decade.

Two areas of national budgeting are held to make available provision the increase in age-related spending: the first is defence spending which has halved since the height of the Cold War; and the second is the cost of servicing our debt which has also halved, despite the level of that debt more than doubling as a share of GDP since the late 70s. This Chancellor has also not cut investment spending in response to the deterioration in the fiscal position in the wake of the pandemic.

The post general election large increases announced in the March 2020 Budget are intended to take total public investment up to its highest sustained level for 40 years. For example, making provision in this Spending Review for improving regional transport links and getting to net zero carbon emissions by 2050.

Fiscal rules

The UK has effectively operated without a fiscal framework since the pandemic began. The Chancellor has repeatedly talked about balancing the current budget to get debt falling as a share of GDP. The Chancellor has now codified his fiscal objectives as rolling targets over the next three years, and a wider set of indicators relating to the affordability of debt.

While the UK is on track to meet the Chancellor’s fiscal rules, this may be by only the slimmest of margins against the headline target of debt falling by 2024-25 with just head room of 0.6 per cent of GDP, which would be easily wiped out by 1% lower GDP growth or 1% higher interest rates.

The UK economy seems to have emerged from the worst of the pandemic relatively unscathed. The OBR say that is this owing no small measure to the extraordinary support over the past 18 months. With the stronger than expected economic recovery, the Chancellor has raised taxes by more this year than any Chancellor since 1993 (and that took two Chancellors) and taken the tax burden to its highest level since the early 1950s.

Anthony Denny

17 December 2021