|

|

|

Denny Sullivan |

|

Telephone:

& also at |

| Economic Outlook - Autumn 2015 | ||||||||

|

|

The Spending Review sets departmental spending limits for each financial year from 2016/17 to 2019/20. While some departments have protected budgets including the NHS, defence and international development, others see larger reductions. Reducing departmental spending forms part of the Government’s plan for reducing the difference between what it receives in taxes and public sector spending; the deficit. Even taking account of reductions in borrowing under the Coalition, the deficit remains high (an expected deficit of £74 billion this year or 4% of GDP) and Government’s aim is to eliminate the deficit. The total stock of debt arising from past borrowing also remains high by international standards at around 80% of GDP.

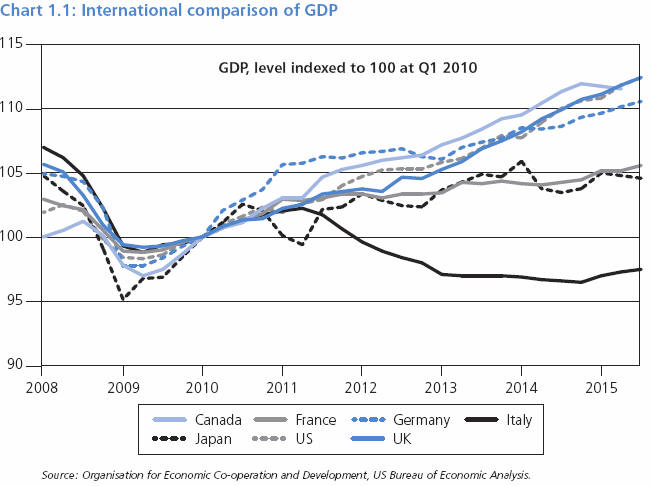

Growth forecast Real GDP growth for 2015 is forecast by the OBR as 2.4% and compares well with the Treasury’s survey of independent forecasts of 2.5% for 2015 (and 2.4% for 2016). Although growth has remained healthy in 2015, a weakness in manufacturing and construction has led to a slight slowdown in the recent quarterly growth rate. The latest OECD forecast expects the UK, along with the US, to have the joint fastest growth rate of the ‘G7 developed economies’ in 2015 (the Eurozone’s growth is forecast as 1.5%).

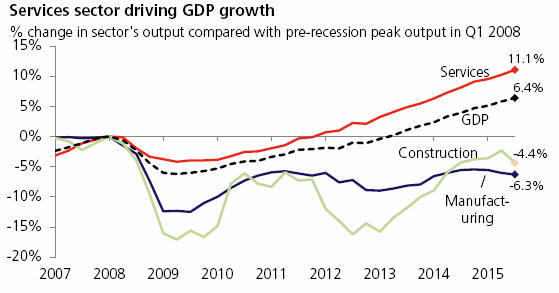

In the near term the likelihood is for continued strong growth in consumer spending owing to rising inflation-adjusted household incomes. In part because of recent wage growth and partly through historically low inflation, at near zero. The services sector (which makes up around four-fifths of the UK economy) continues as the main driver of growth. There was strong quarterly growth in transport, storage and communications, and business services and finance sectors. In contrast, the construction sector (6% of the whole UK economy) saw a sharp quarterly decline in output. Activity in the manufacturing sector (10% UK economy) declined for the third quarter in succession, while output in oil and gas rose. This divergence in growth continues the widening gap in performance since 2008 between the services sector on the one hand and manufacturing and construction sectors on the other.

The 2008/2009 crash had a much greater impact on the manufacturing and construction sectors than on the services sector and the recovery in services has been much stronger and the most important factor in the UK’s economic recovery. Output in services industries was over 11% higher in 2015 compared with the 2008 pre-recession peak, contrasting with output from the manufacturing sector that is over 6% lower than 2008, while output from the construction sector is over 4% below that of the pre-recession level. Since the recovery began, economic growth has been supported by domestic expenditure, mainly consumer spending and investment. Whereas net trade, the difference in exports and imports to the UK, has generally been a drag on growth in recent years. Accordingly the main risks to the UK’s economic growth comes from the international economic outlook and the possibility that UK productivity growth fails to recover. Office for Budget Responsibility’s forecast

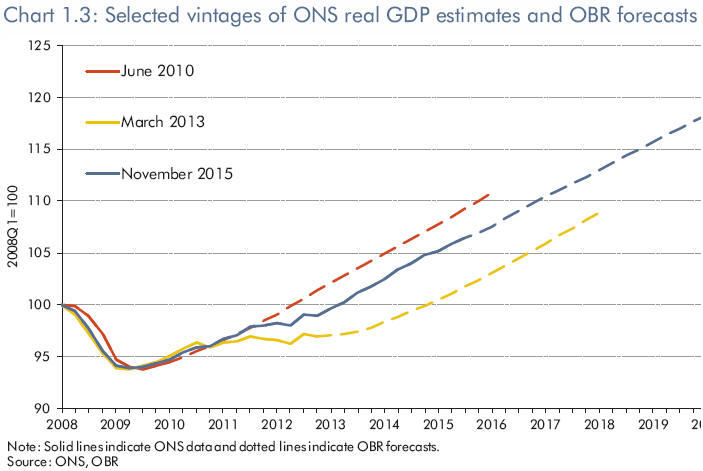

The starting point for the OBR forecast is the revised real growth rates reported by the Office for National Statistics (ONS). According to this the broad picture of recent annual growth of the UK economy, over the last five years, remains very healthy and indeed close to their 2010 forecast for growth:

Productivity and potential output of UK economy Prospects for productivity growth represent the most important uncertainty in the OBR’s forecast for the UK economy. According to the Treasury, UK productivity has for decades lagged behind other major economies and in 2014 output per hour remained 20 percentage points below the G7 average. Productivity directly links to living standards and the UK’s ability to improve living standards is dependent on productivity growth. In the UK, productivity is reported to have been growing at an historical average rate of around 2% a year in the decade prior to the crash.

Since then productivity fell and has failed to recover. The ONS describing this stagnation as “unprecedented in the post-war period”. Recently the ONS has reported an improvement, the first two quarters of 2015 saw a pick-up in productivity growth. A key assumption in their forecasting therefore is that the OBR expect an acceleration in productivity growth, a return to 2% annual productivity growth by the end of 2016.

Inflation and monetary policy Headline inflation is at present very low with prices generally falling over the year to October. The CPI measure is now minus 0.1% and has been very low for most of 2015, fluctuating between +0.1% and -0.1% since February. The level of inflation is also lower than in recent years, averaging 2.6% in 2013 and 1.5% in 2014.This historic fall in inflation is largely owing to the fall in the oil price and lower food prices.

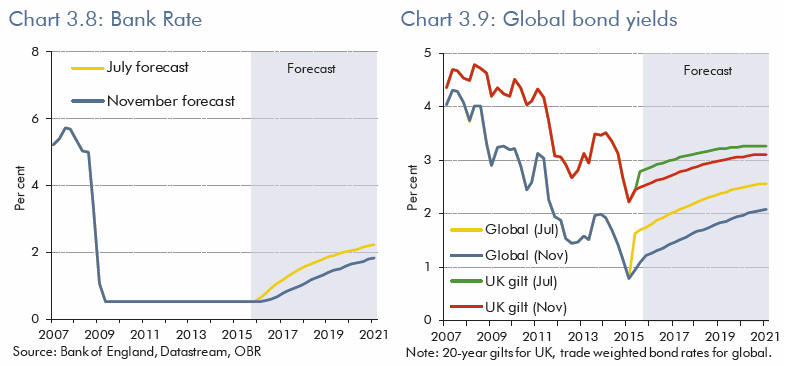

The UK is not alone in experiencing very low inflation, or deflation. Eurozone inflation was plus 0.1% in October, from minus 0.1% in September, and inflation in the US was minus 0.7% over the year to August 2015. The outlook is for inflation to continue to remain low and be so almost certainly for the rest of this year and into next. The Bank of England’s Monetary Policy Committee (MPC) has kept the base rate at the historically low level of 0.5% since March 2009. The MPC tends to focus on the underlying drivers of inflation that have unemployment falling and wage increases strengthening. Their attention is turning to the possibility of when interest rates might begin to rise. The MPC voted (November ‘15) 8-1 in favour of maintaining interest rates at 0.5% and following publication of the Bank of England’s November Inflation Report the general expectation is for there to be no change in interest rates until the end of 2016 or even possibly 2017. The Governor of the Bank of England has said that the position will be clearer around the turn of this year. Commentators believe the Bank has given an unambiguous signal that any interest rate rise has been delayed around a year to late 2016 and according to the FT: ‘the market is not pricing in the first interest rate rise until early 2017’. The weakening of the global economy, especially emerging markets, is one factor behind the change to the expected timing of the rise in interest rates. Although interest rates are likely to remain lower for longer the Bank has indicated that tighter lending rules may be considered to prevent excessive borrowing destabilising the UK economy.

Labour market The UK labour market continues to surprise and following a dip in 2011, UK employment has been growing strongly since spring 2013, through 2014 and into 2015, to reach a record historic high of 31.21 million people (73.7% of people aged from 16 to 64), an increase of 419,000 people in work compared to the previous year. The highest rate of employment since comparable records began in 1971.

There is now (July-September 2015) over 2.1 million more people in work than in the 3 months to April 2010. Excluding people above the state pension age, the employment rate is nearly the same as in late 2007 at 75% of the working age population. The unemployment rate is now very close to the pre-crash level at 5.3% of the economically active population who are unemployed. Average earnings growth accelerated in the first half of 2015 and earnings are now growing at a faster rate than during the previous five years. However they are increasing more slowly than before the recession, suggesting there is still a capacity in the UK economy for faster earnings growth.

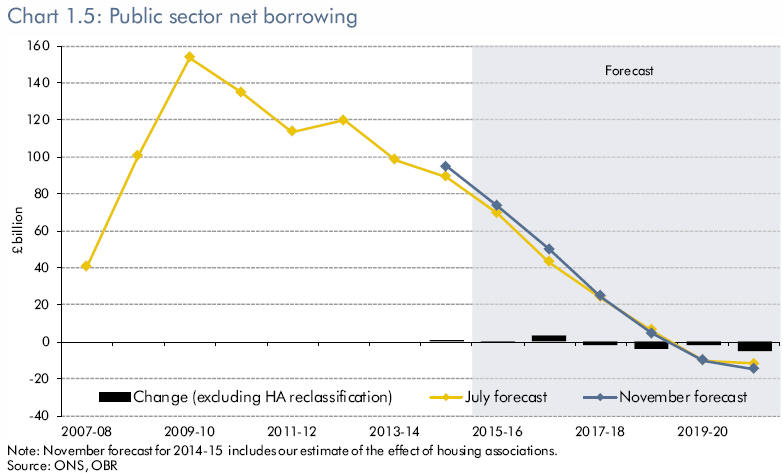

Average weekly pay increased by 3% including bonuses in the year to July-September 2015 and by 2.5% excluding bonuses. Inflation, as measured by the CPI, averaged zero over the same period. The OBR expect employment growth to slow as productivity growth recovers. Public finances Government believes significant progress was made over the course of the last Parliament in mending public finances. Public sector net borrowing, the difference between Government’s spending and revenues, was £153 billion (10.2% GDP) in 2009/10, but reduced to around £90 billion last year 2014/15.

The annual rate of borrowing moves from an expected deficit of £74 billion this year 2015/16 to a surplus of £10 billion in 2019/20. The OBR expect the deficit to fall more sharply over the rest of this year than it has to date. Even with the fall in UK government borrowing over recent years, it remains high by international standards. Borrowing to fund the UK’s deficit, will be around 4% of GDP in 2015, similar to that of France, but higher than in Italy, Canada or Germany.

The national debt, or public sector net debt, at March 2015 is recorded as £1,487 billion (in scale, 80% of GDP).

Public spending In the first combined Spending Review and Autumn Statement since 2007, the Government has taken advantage of an improvement in the apparent outlook for tax receipts (the self-employed in particular) to further loosen the impending squeeze on public services spending, to increase capital spending and to reverse the, politically unpopular, main tax credit cuts. Compared to the Summer Budget 2015, the OBR now forecasts higher tax receipts and lower debt interest, with a £27 billion total improvement in the public finances across the whole forecast period, making possible a ‘smoothing’ of the path and reduction in the amount of ‘austerity’ intended by the Coalition.

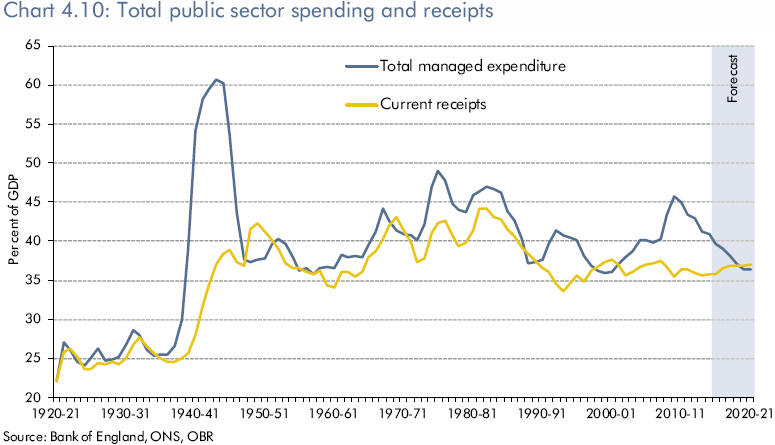

In 2015/16, Total Managed Expenditure (all public spending) is expected to be £756 billion, 40% of GDP, marginally below the average over the last 60 years (from 1955/56 to 2014/15) of 41% of GDP. It is forecast to fall to 36% of GDP in 2019/20.

The three biggest sources of change over the next four years are receipts, welfare spending and departmental budgets:

These plans for spending in aggregate reduce the squeeze on public services spending planned for this Parliament, implying real cuts more than a third smaller on average than those delivered over the last Parliament and around two thirds smaller than those pencilled in by the Coalition back in March ‘15. In making these changes the fiscal tightening has been reduced from around 1.6% (in real terms) a year in the last Parliament to a projected 1.1% reduction each year in real terms, which some have commented is in contrast to the rhetoric of austerity.

Anthony Denny November 2015 |

|||||||